The Hidden Risks and Rewards of Investing in Off-the-Plan Developments (2025 Edition)

Before you buy off-the-plan, discover what smart investors know—and others don’t.

Josh Tay

Josh Tay

Have you ever wondered why so many people are suddenly talking about off-the-plan properties again?

Maybe you’ve seen ads that promise “high returns,” “prime city views,” or “guaranteed rental income.”

Maybe a friend just bought one and said, “You should too before prices go up.”

But before you swipe your card or sign that reservation form — let me be real with you. Off-the-plan projects can make you wealthy… or keep you waiting. They can deliver beautiful, brand-new homes… or endless delays and sleepless nights.

I’ve been in the property industry long enough to see both sides — the buyers who made six-figure gains and the ones who couldn’t even settle because banks cut valuations.

So today, I’m here to tell you what most agents won’t.

Let’s talk about the real risks and the hidden rewards of buying off-the-plan in 2025. Because if you play this right, it could be your smartest move this decade. But if you don’t… it might be the costliest.

What’s Really Happening in Australia’s Property Market (As of October 2025)

Australia’s property market has been through quite a ride.

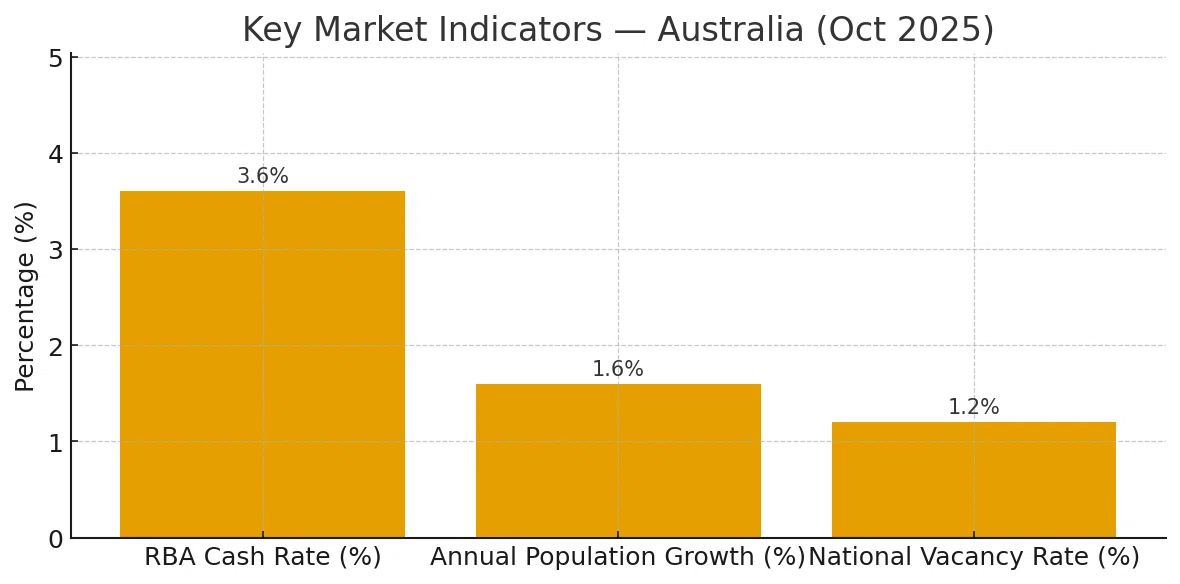

- Interest rates have stabilized at 4.35%, and the Reserve Bank is hinting at a possible cut in early 2026.

- Population growth is booming again, especially in Melbourne and Perth, as migration surges back to pre-pandemic levels.

- Rental demand remains sky-high — with vacancy rates below 1% in most major cities.

- And construction costs? They’re finally easing after two brutal years of inflation.

That combination — lower construction costs, strong rental demand, and stable lending — has sparked a new wave of off-the-plan launches across Australia.

Developers are back. Investors are circling. And the question everyone’s asking is: “Is it worth buying off-the-plan in 2025?”

Let’s unpack this carefully.

The Rewards: Why Smart Investors Still Love Off-the-Plan Properties

1. You Lock In Today’s Price — While the Market Grows

This is the golden rule of off-the-plan investing. You pay a small deposit now (usually 10%), and the rest only upon completion — often 2 to 3 years later. If the market rises in that time (and it usually does in Melbourne and Perth), you could be sitting on instant equity the day you settle.

For example: That’s a $60,000–$100,000 gain before you even move in or rent it out. |

That’s why seasoned investors love pre-construction buys — it’s like time working in your favor.

2. Brand-New Property = Low Maintenance and High Tenant Demand

Tenants today want modern finishes, smart layouts, and energy efficiency. They’ll pay more for new, especially if it’s close to transport, universities, or shopping areas.

New apartments typically attract 10–20% higher rents than older units in the same suburb. And because everything’s brand-new, from the appliances to the plumbing, your maintenance cost is close to zero in the first few years.

For busy investors or those planning to migrate or retire, that’s peace of mind money can’t buy.

3. Tax Benefits and Depreciation

If you’re investing, this is where it gets juicy.

New builds allow you to claim maximum depreciation deductions, on both the building and the fixtures. That can mean thousands of dollars in annual tax savings, especially if you’re renting it out.

In Australia, new properties can be depreciated over 40 years, giving you a steady buffer against your rental income.

4. Flexibility — and Time to Plan

Buying off-the-plan gives you breathing room. You don’t have to rush your finances now. You can use the construction period to restructure your loans, plan your migration, or even sell another property first.

For many Singaporean families buying for children’s education or retirement, this timeline is a gift — not a risk.

The Risks: What You Must Know Before Signing Anything

Now, let’s talk about the part nobody likes to discuss. Because off-the-plan investing isn’t a fairytale — and if you go in blind, it can hurt.

1. Construction Delays and Developer Defaults

Let’s be honest: this is the biggest risk.

In 2024 alone, several Australian developers — even big ones — went under due to rising costs and cash flow issues. While conditions have improved in 2025, delays of 6 to 12 months are still common. That means if your settlement was due mid-2025, it might get pushed to 2026. And if a developer collapses mid-project, your contract could be terminated, and while your deposit is usually protected, your time and opportunity aren’t.

My tip: Always check the developer’s past track record — how many projects they’ve actually completed. Don’t fall for glossy renders or celebrity endorsements. Look for substance.

2. Valuation Shortfalls

This one’s sneaky.

By the time your property is complete, the bank sends a valuer. If the market hasn’t moved up as much as expected, or if too many similar units hit the market, your property might be valued below your purchase price.

For instance:

You agreed to buy at $800,000 in 2023, but by 2025 the valuer says it’s worth $760,000. The bank will lend you less — and you’ll need to top up the difference in cash.

This is where many first-time buyers panic.

My advice: Have a buffer. Always. And work with a realtor who can help you revalue, negotiate, or even resell before settlement if needed.

3. Market Saturation in Certain Suburbs

Not every suburb is created equal.

Some inner-city pockets — especially in Brisbane and Sydney — are oversupplied. But in Melbourne’s west (like Footscray, Sunshine, and Werribee) and Perth’s northern corridor (like Joondalup and Clarkson), demand still outweighs supply.

The key is knowing which pockets are undersupplied and where rental growth is strongest. That’s where you get the upside.

4. Interest Rate Sensitivity

If rates go up before your project completes, your borrowing power might drop.

But the good news? Australia’s rates are expected to ease in 2026, and fixed-rate options are becoming more flexible again. So while it’s a risk, it’s also a short-term one.

Where the Smart Money is Going: Melbourne and Perth

If you’re looking for where the real opportunity lies in 2025 — two cities stand out.

Melbourne — The Comeback City

- Melbourne is roaring back stronger than ever.

- Population is expected to hit 6 million by 2026, overtaking Sydney.

- Vacancy rates are below 1%, and rents have jumped over 20% year-on-year in some inner suburbs.

- Education demand remains massive, with University of Melbourne, RMIT, and Monash driving global migration.

Off-the-plan apartments near city fringes like Southbank, Brunswick, and Footscray are seeing early buyers already in profit.

In my opinion, Melbourne offers the best long-term value — a mix of lifestyle, culture, and capital growth.

Perth — The Underrated Goldmine

If Melbourne is the comeback, Perth is the quiet goldmine. It’s affordable, growing fast, and still underpriced compared to every other capital city.

- Median house price (Oct 2025): A$720,000, still 30–40% lower than Sydney or Melbourne.

- Vacancy rate: 0.6% — the tightest in the country.

- Rental yields: as high as 5.5–6% for new apartments.

- Migration from the east and overseas is accelerating.

Developments around Joondalup, Scarborough, and Perth CBD are now getting global investor attention — and rightly so.

I’ve personally seen clients double their rental income within two years of completion.

If you’re an investor who missed the Sydney and Melbourne boom ten years ago, Perth is your second chance.

Who Should (and Shouldn’t) Buy Off-the-Plan

Off-the-plan properties are not for everyone.

They’re great if you:

- Want to build wealth passively over time

- Prefer brand-new, low-maintenance homes

- Plan for education, migration, or retirement

- Are okay with a 2–3 year waiting period

But they’re not ideal if you:

- Need quick rental returns immediately

- Don’t have extra savings for potential top-ups

- Panic easily when markets fluctuate

It’s all about matching the right project to your goals. And that’s where having an experienced realtor makes all the difference.

My Honest Opinion (After 15+ Years in This Game)

If you’re a Singaporean or overseas investor looking for stability, growth, and lifestyle, Australia — especially Melbourne and Perth — still delivers some of the safest and most rewarding opportunities in 2025.

But don’t rush.

The worst thing you can do is buy the wrong project from the wrong person.

Instead, let’s take this step strategically. Let’s review the developer, the suburb, the rental demand, and even the resale history around it.

Because when done right —

- Off-the-plan can multiply your wealth,

- Future-proof your family’s lifestyle, and

- Secure your place in one of the world’s most livable countries.

Don’t Miss This Window: Let’s Talk Before You Miss Out

The next 12 months are crucial.

With Australia’s construction costs cooling and interest rates likely to drop in 2026, prices are expected to rise again.

That means the best time to lock in an off-the-plan price…is now — before the market catches up.

If you’re serious about securing your family’s future through Australian property —especially in Melbourne or Perth — I’d love to help you personally.

Let's talk! Contact me today!